Debt-ceiling negotiations stalled

BY Janne Muta

|maggio 24, 2023US equities traded lower yesterday as negotiations over the debt ceiling continued to create uncertainty. Treasury Secretary Janet Yellen has issued a warning, cautioning that a potential default could occur as early as June 1. This impending deadline adds to the mounting pressure and anxiety surrounding the debt ceiling negotiations. Despite ongoing discussions, yesterday's meeting between President Biden and McCarthy ended without a deal.

The debt ceiling impasse in Washington has triggered a safe-haven effect, with investors flocking to the USD. Also, hawkish Fedtalk has further boosted the dollar's strength, even in the face of potential default and recession risks. Market participants are now anticipating that interest rates will remain elevated for the time being. The release of the FOMC Minutes in the US session today reveals more about Fed bankers’ thinking.

As earnings season winds down, a remarkable 77% of S&P 500 companies have surpassed consensus expectations. This impressive performance can be attributed to better-than-anticipated revenue growth, economic resilience, and cost-control initiatives implemented by companies across various sectors. The markets, however, focused on the near-term risks. Ten out of eleven S&P 500 sectors ended the day in the red. The only sector to gain was the energy sector (1.09%). Basic materials, technology and telecommunication sectors were the biggest losers shedding 1.55%, 1.48% and 1.24% respectively.

The annual UK April headline inflation (8.7%) declined compared to March (10.1%), but the focus should be on the core annual inflation figure, which increased substantially (+6.8% vs +6.2% y/y expected). Price pressures are still strong in the UK economy. While food price inflation remains high with only a slight decrease, the drop in headline annual inflation is primarily due to base effects following last year's surge in energy prices. The core annual inflation rate is currently at its highest level since March 1992.

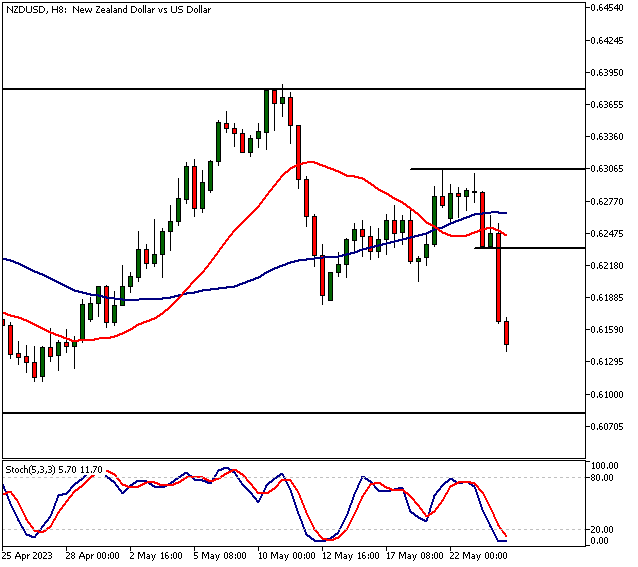

The NZD took a dive today, dropping 1.3% after the Reserve Bank of New Zealand signalled an end to rate hikes. The Reserve Bank of New Zealand (RBNZ) rate hike was in line with expectations. The central bank raised interest rates by 25 basis points and surprised the markets with a dovish overall tone and guidance. This triggered a sell-off of more than 1.3% in NZD.

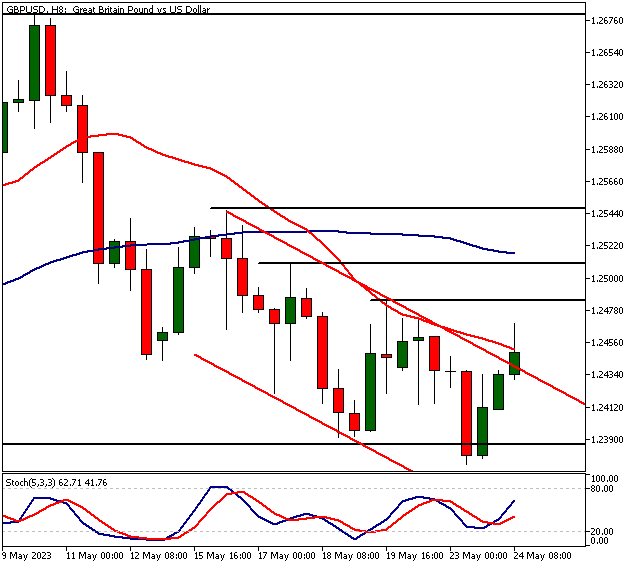

GBPUSD

GBPUSD rallied as the CPI numbers showed the price pressures remain in the UK economy. The market tries to break out of the bearish channel and could turn bullish above 1.2446. Above the level, look for a move to 1.2480 and then to 1.2415 on extension. Below 1.2446, the market might move to 1.2380.

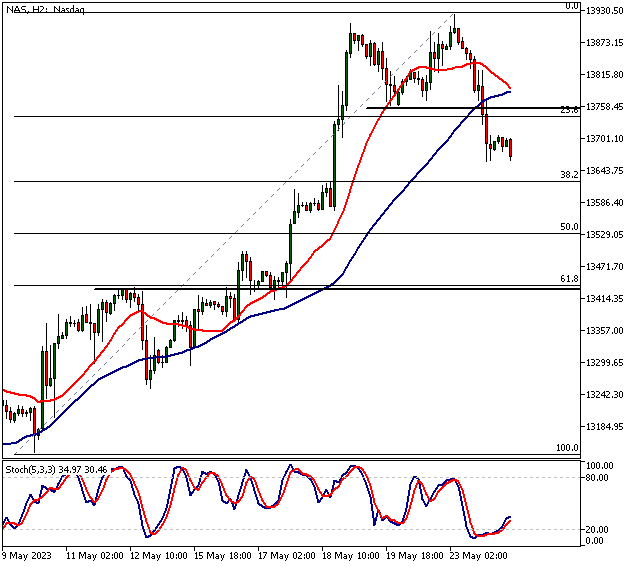

NAS

Nasdaq is short-term bearish below 13 760 after yesterday’s bearish engulfing candle. Below 13 760 the market probably trades to 13 630 and then possibly to 13 500 on extension. Above 13 760, look for a move to 13 890.

NZDUSD

NZDUSD is bearish below 0.6233 after the RBNZ decided to hike only 25 bp (25 bp expected) which was already priced in. The central bank was also quite dovish in its forecasts and messaging. Below the level, we might well see a move to levels near the lows of the recent range. The market might move to 0.6080 or so. If the level doesn’t hold, look for a move to 0.6000 on extension. Above 0.6233, NZDUSD could trade to 0.6290.

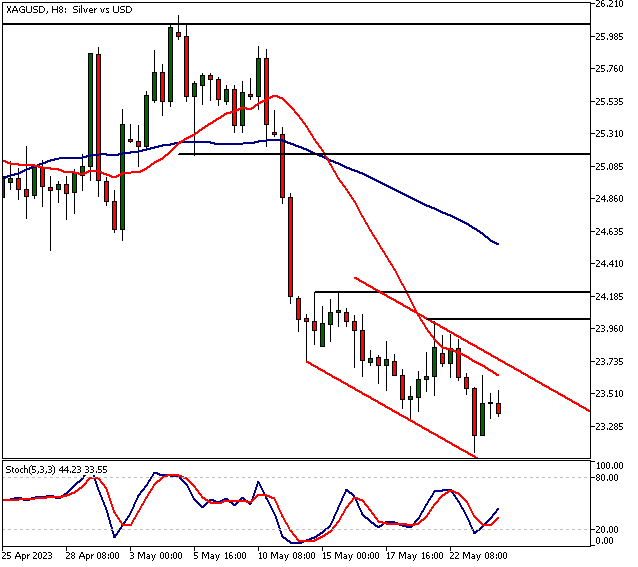

Silver

Silver is bearish below 23.64 and might trade down to 22.70. Above 23.64, look for a move to 24.10. Silver has a fairly high correlation to gold so if the fall in the US 10-yr. yield continues today both precious metals could appreciate.

The Next Main Risk Events

- EUR German IFO Business Climate

- GBP BOE Gov Bailey Speaks

- GBP BOE Gov Bailey Speaks

- USD Treasury Sec Yellen Speaks

- USD FOMC Meeting Minutes

- USD Prelim GDP

- USD Unemployment Claims

- USD Prelim GDP Price Index

- USD Pending Home Sales

- JPY Tokyo Core CPI

- GBP Retail Sales

- USD Core PCE Price Index

- USD Core Durable Goods Orders

- USD Durable Goods Orders

- USD Revised UoM Consumer Sentiment

For more information and details see the TIOmarkets economic calendar.

Trade Safe!

Janne Muta

Chief Market Analyst

TIOmarkets

DISCLAIMER: TIOmarkets offers exclusively consultancy-free service. The views expressed in this blog are our opinions only and made available purely for educational and marketing purposes and do NOT constitute advice or investment recommendation (and should not be considered as such) and do not in any way constitute an invitation to acquire any financial instrument or product. TIOmarkets and its affiliates and consultants are not liable for any damages that may be caused by individual comments or statements by TIOmarkets analysis and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his/her investment decisions. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances, or needs. The content has not been prepared in accordance with any legal requirements for financial analysis and must, therefore, be viewed by the reader as marketing information. TIOmarkets prohibits duplication or publication without explicit approval.

Janne Muta holds an M.Sc in finance and has over 20 years experience in analysing and trading the financial markets.

Related Posts

Trade responsibly: CFDs are complex instruments and come with a high risk of losing all your invested capital due to leverage.